Time is perhaps the most influential piece in the financial planning puzzle. In his days, Albert Einstein contributed extensively to humanity’s understanding of the complexities of time, and he has provided some of the absolute best, uncomplicated, explanations of what time is and represents.

A couple of examples include, “time is what clocks measure,” and “the only reason for time is so that everything doesn’t happen at once.”

Einstein also demonstrated in proof form that time and space—the dimensions, position, and momentum of objects–are inextricably connected and help to define each other. That the interaction of objects in space and time is infinitely more complex and elegant than the practical, linear, concept of time we cycle each day.

In the world of portfolio management, we frequently explore the profound connection between time and risk and their influence on each other. Like time, risk is a continuum bent and formed by the gravity of every investor’s unique position. And like risk, time governs the amplitude of our human experience.

The Human Experience: Journeys and Moments

Human lives consist of journeys and moments. Typically, individual moments carry a relatively minor effect on the outcome of a journey although, collectively, they form the journey’s entirety. When we think of journeys, it is natural to think of travel and air travel, specifically. Air travel serves as a very useful analogy for illustrating the relationship between time and risk.

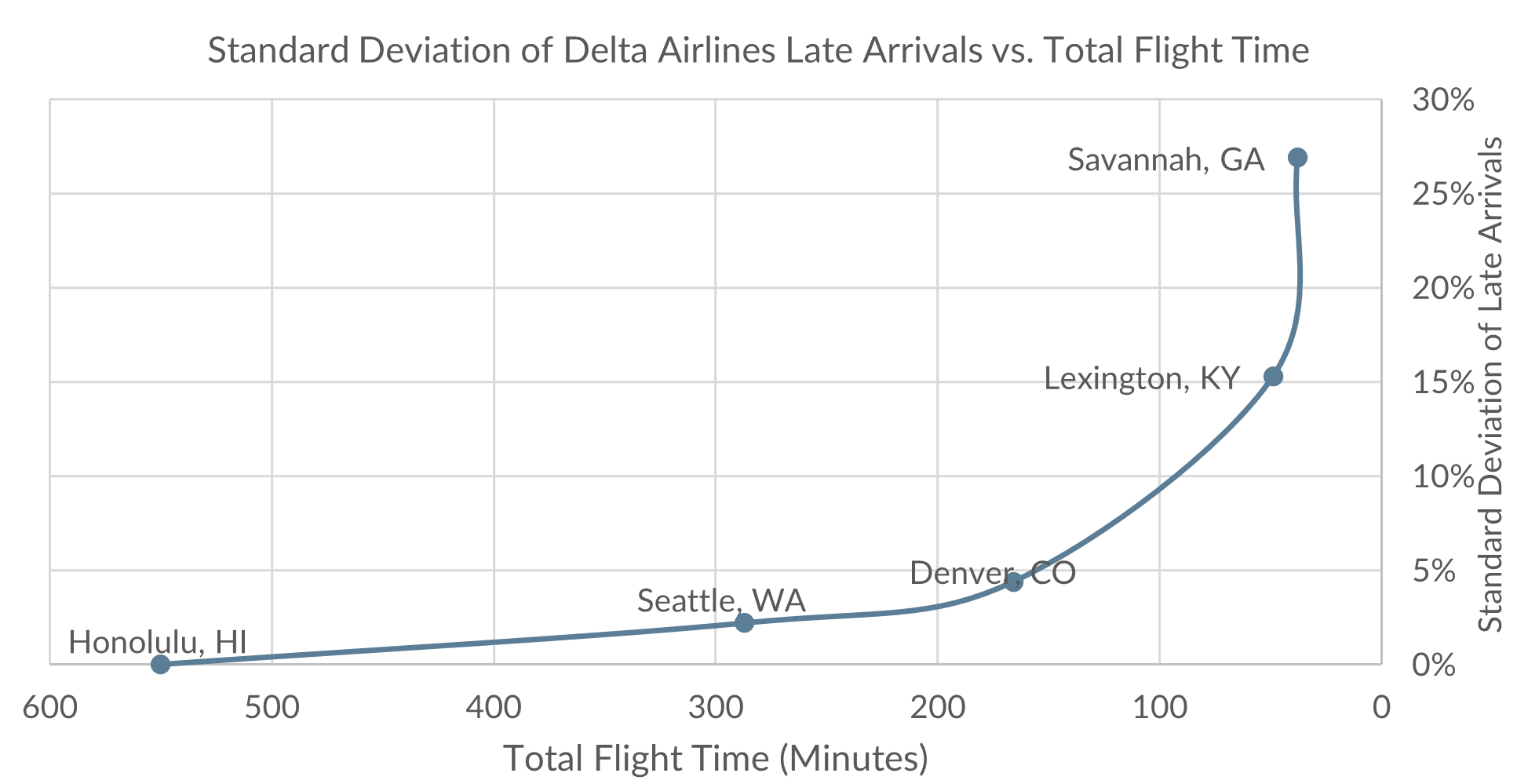

Safety is, of course, the chief concern when traveling by air, however, on-time arrival is also critical to a positive travel experience. Delta Airlines data from 2022 reveals that those flights with the shortest total flight duration faced the greatest risk of a late arrival versus flights with longer total durations. The concept of standard deviation is a statistical term used to describe how spread-out data is. In this example, the data is the extent of a flight’s late arrival expressed as a percentage of the flight’s total duration.

The standard deviation of late arrivals among Delta flights between Atlanta and Lexington was 15% whereas the standard deviation of late arrival flights between Atlanta and Seattle was a mere 3%. In layperson’s terms, this means a passenger travelling from Atlanta to Lexington has a 95% chance of arriving between 8 minutes early and 10 minutes late. A passenger travelling from Atlanta to Seattle has a 95% chance of arriving between 9 minutes early and 11 minutes late. These are similar figures in terms of absolute minutes, however, the average airborne time for the Seattle route is 7.5x longer than the Lexington route—287 minutes versus 38 minutes. The relative impact of a delay for Seattle passengers was much smaller.

As the journey lengthens, the relative influence of individual moments on the outcome diminishes. While there are undoubtedly exceptions, both positive and negative, this doesn’t imply that single moments are inconsequential. Rather, it suggests that the passage of time allows for adjustments when challenges arise and enhances growth when things are progressing favorably. Moments are very important, as well.

Certain moments play a pivotal role in defining our existence. When contemplating examples of the culmination of a person’s relentless pursuit, my thoughts invariably drift towards Olympians. A prime example of the weight carried by singular, transformative moments in our lives can be seen in the immense pressure endured by Olympic gymnast Gabby Douglas. Over a decade of dedication and training was distilled into a mere 90 seconds on the balance beam during the 2012 Olympic Games. That defining instance, where she clinched both the team and all-around gold medals, was momentous. Investors, similarly, encounter crucial junctures in their financial planning journey, and abbreviated time frames amplify both the likelihood and potential repercussions of hazardous events.

Time, Risk, and Investing

Like elite athletics, successful investing outcomes result from long-term execution of planning, monitoring, and disciplined performance under pressure.

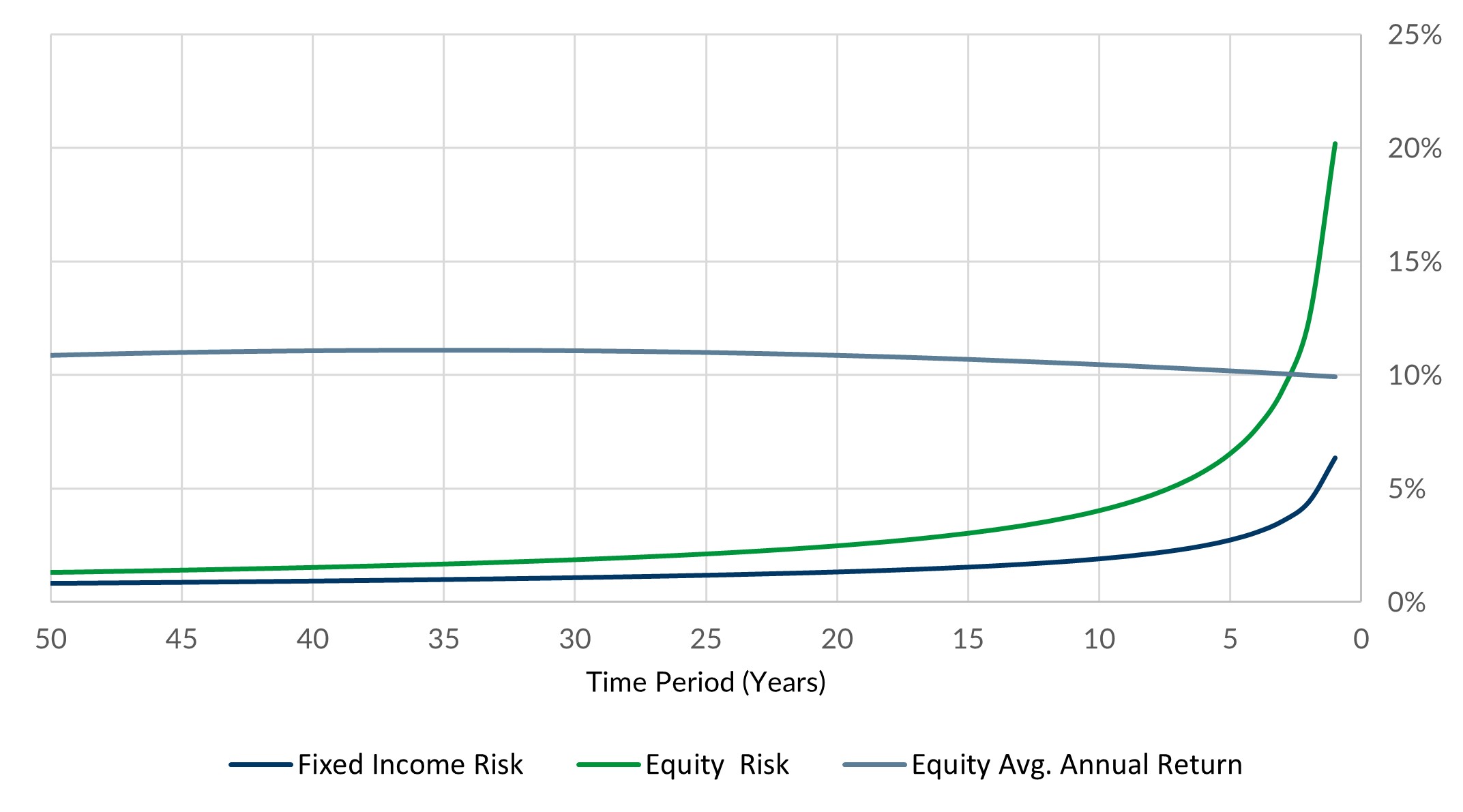

Time bends risk the longer our time horizon is but magnifies risk the closer we get to monumental moments. The holding period of an investment substantially affects its volatility, as measured by the standard deviation of the investment’s returns. For instance, the annualized volatility of an equity investment over a 1-year period is about 20x higher than the volatility over a 50-year period. Even the volatility of a 1-year period versus a 10-year period is 5x higher.

Time’s effect on risk conjures a variety of approaches for investors with varying time or risk horizons. Goal-oriented investors often pursue strategies geared toward discrete time-oriented goals, whereas generational or institutional investors may pursue goals that are naturally more open-ended with varying or segmented time and risk horizons. Some investors may present a shorter perceived time horizon, but require a much longer risk horizon; however, others may present a longer perceived time horizon, but require a shorter risk horizon.

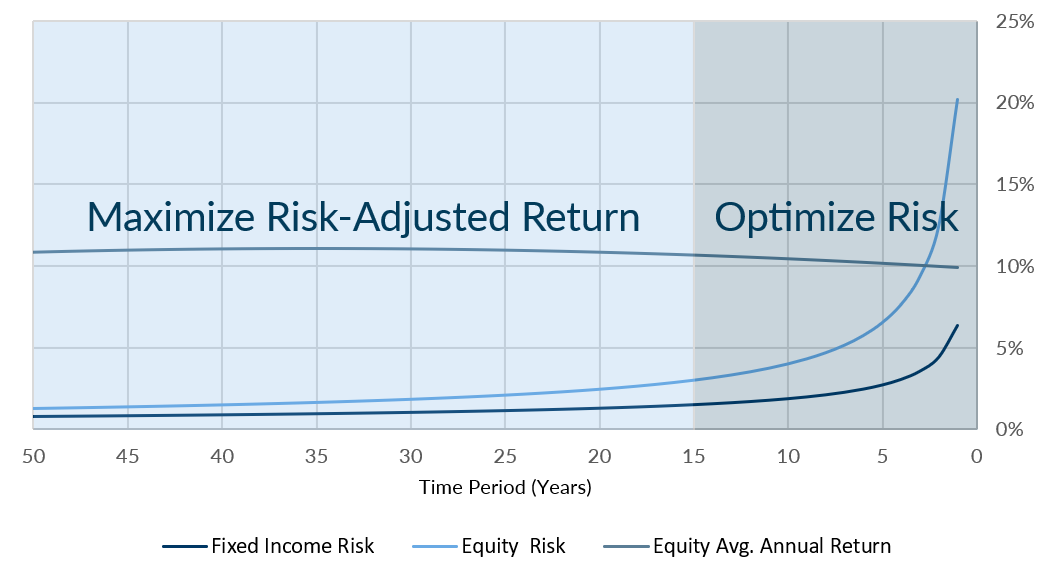

From an investment solution standpoint, this presents two clear opportunities: maximize the risk-adjusted long-term return for investors on the longer end of the time or risk horizon and optimize risk-adjusted return for investors on the shorter end. By optimizing portfolios to maximize risk-adjusted returns using longer-holding period risk and return assumptions, investors on the longer end of the time and risk horizon may become more naturally suited to a return space that may traditionally be otherwise too aggressive. On the other hand, by optimizing portfolios using shorter-term risk and return assumptions, investors on the shorter end of the time and risk horizon may become better candidates for a return space that may be traditionally otherwise too conservative.

Ultimately, this framework supports the utilization of asset allocations that evolve smoothly over time as well as the use of asset classes and investment management styles that correspond closely to the unique attributes of the various investors sitting along each interval of the time and risk horizon.

Closing Thoughts

The pillars of portfolio management are asset selection, asset allocation, and asset monitoring. The long-term experience of any investor consists of the specific investments they hold, how capital is allocated across those investments, and how asset allocations are adjusted over time.

By exploring the effects of time and risk American Trust:

- Tailors access to asset classes and investment styles that encompass the entire return space of what is opportune and prudent for each client based on their unique time and risk horizons.

- Constructs investment portfolios that not only diversify risk based on near-term expectations but customize portfolio diversification according to the investor’s specific time and risk horizons.

- Addresses the needs of all clients, whether they are goal-oriented investors with discrete time horizons or generational investors with more open-ended sets of goals.

American Trust Wealth is proud of its fiduciary heritage and remains focused on the advancement of its time-tested fiduciary and investment processes and the delivery of positive client outcomes. We are honored to manage the assets of our clients and we understand the reality that the money we manage represents the product of a lifetime of journeys and moments, as well as the future of our clients and their households.

As always, please do not hesitate to contact your Fiduciary Investment Advisor should you have any questions or updated wishes concerning your financial and investment planning.