November is a magical time around the American Trust office in Lexington, KY. Crisp autumn air engulfs the Bluegrass. Amber and saffron foliage blankets the horizon. The sweet smell of cracked corn and sour mash permeates the river valleys. And, this November, the thunderous roar of hooves and the betting public cheering them on were the toast of the town.

Lexington was honored to host some of the finest thoroughbreds in the world during the Breeders’ Cup World Championship and one special horse, Flightline, had a banner week. The Kentucky-bred bay colt first dismantled a talented field of, mostly former Derby, horses and then made history when a 2.5% share in its breeding rights sold at auction for $4.6 million representing a total valuation of $184 million.

As we reflect on that experience and the international flair accompanying it, it’s hard not to contemplate at least some of the potential implications our local experiences may have for the world beyond. Inflation, perhaps?

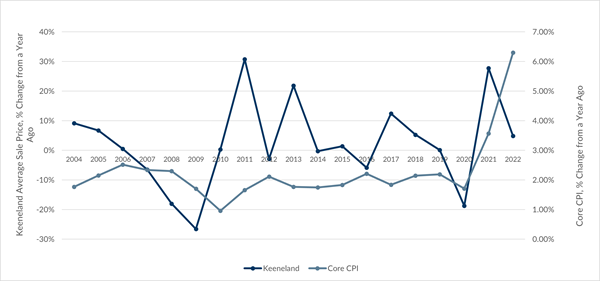

THE KEENELAND SALES PRICE INDEX

The Keeneland Thoroughbred Auction House hosts four Thoroughbred sales annually and publishes an exhaustive record of its results. The horse racing industry is, perhaps second only to Major League Baseball, notorious in its stat-keeping. While aggregate sales are still climbing back from pre-financial crisis highs, the sale price trends are intriguing.

In fact, the average “price per head” is on the rise and is on track to hit an all-time high north of $100,000 per head in 2022 compared to an average pre-pandemic price of $77,000 and an average pre-financial crisis level of $90,000.

What, if any, implications do increasing thoroughbred sales prices have for broader price levels? By indexing the thoroughbred sales data and evaluating the annual change in prices, it’s possible to draw comparisons with broader economic indicators such as the Consumer Price Index (CPI) and inflation. We find annual changes in the average sales prices from the prior year are moderately correlated with annual changes in the CPI over the following year. What does this mean?

Simply put, it means there is a statistical basis for the notion that thoroughbred sales prices in one year may serve as a leading indicator for the CPI and inflation the following year.

For example, the annual change in sales prices increased substantially in 2017 and the CPI followed with a gradual rise between 2017 and 2019. In 2021, the annual change in sales prices rocketed by 28% and yet again, the CPI has followed with sizeable increases in 2021 and year to date. Interestingly, the sale prices have tapered somewhat increasing by about 5% in 2022. Might this mean a slowing rate of inflation for the broader economy next year?

It will be fun to keep tabs on this carnival indicator in the months ahead to see if the “hips (numbers) don’t lie”, however, with the Keeneland sales prices explaining just over 15% of the variation in the CPI at just 90% confidence, it is unlikely the American Trust investment team will introduce the metric into canon just yet.

AN INFLATION REFRESHER

As a reminder, the Consumer Price Index (CPI) is a monthly measure of the prices paid by U.S. consumers for goods and services. The Bureau of Labor Statistics (BLS) calculates the CPI by evaluating the weighted average prices for a basket of consumer goods and services representative of total consumer spending. Inflation is a result of rising prices of goods and services as measured by an increasing CPI.

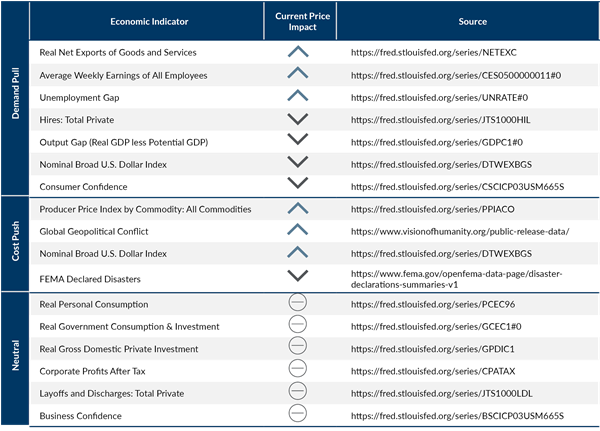

Inflation is influenced in three primary ways:

- Demand-pull Inflation – Inflation resulting from aggregate demand growth outpacing growth in aggregate supply.

- Cost-push Inflation – Inflation resulting from increased production costs and decreased aggregate supply.

- Inflation Expectations – Inflation resulting from potentially self-fulfilling prophecies regarding future inflation which may accelerate future behaviors to the present time.

Below is a snapshot of the underlying metrics driving these forms of inflation as well as their current inflationary pressure or impact.

INFLATION OUTLOOK FOR 2023

Inflation is of economic importance because of its cascading effects. First, inflation is a serious factor for both fiscal and monetary policy. Central banks worldwide have adopted formal policies targeting maximum employment and price stability. Increased prices reduce purchasing power, erode the value of existing savings, discourage future savings, and can even reduce investment and employment.

In November, the Federal Reserve took swift action to curtail recent inflation increases by raising the federal funds rate by +0.75% to a target range of 3.75-4.00%, the highest range since before the financial crisis. Fed funds futures suggest rates will likely increase to at least a target range of 4.75%-5.00% by next March.

Inflationary pressures, as summarized above, appear relatively balanced at this time. This combined with the anticipated impact of the Fed’s ongoing quantitative tightening actions should further reduce inflationary pressures. We remain vigilant over the impact these actions may have on financial markets and client accounts, yet optimistic with the prospect of improved price stability in 2023 and beyond.

As always, if you have any questions, please don’t hesitate to reach out to your Fiduciary Investment Advisor.