As the crisp autumn air approaches, we’re reminded of the simple joys that this season brings. The leaves transform into a tapestry of reds and golds, and communities gather for timeless traditions like hayrides, pumpkin carving, and visits to apple orchards. There’s something profoundly satisfying about strolling through rows of apple trees, surrounded by fruit that’s the culmination of many seasons of care.

These orchards are more than just scenic backdrops for family adventures; they are living legacies—yielding nourishment and enjoyment for generations.

An orchard doesn’t flourish overnight. It demands thoughtful planning, patience, and a steady hand to nurture saplings into mature trees laden with fruit. Each harvest is a testament to the foresight and diligence of years past. The cycles of planting, growth, and harvest offer a natural rhythm that mirrors the principles of income investing.

Just as orchard keepers cultivate their trees to ensure a bountiful harvest season after season, investment managers can design portfolios that yield steady income over time. The rewards are enduring—a reliable stream of income that, like the orchard’s produce, can be enjoyed and consumed, providing sustenance now and for the future.

In the spirit of the season, let’s explore how the art of cultivating orchards parallels the strategies of income investing. We’ll delve into the mechanics of building income-generating portfolios and introduce our new Income Models designed to help you harvest financial stability and growth in your journey.

The Diverse Faces of Income Investors

Income seeking investors span a broad spectrum. They include individuals approaching retirement, aiming to generate sufficient income to replace their paychecks; institutions like foundations and endowments requiring consistent cash flow to meet financial obligations; and even younger investors who prefer the steadying effects of dividends and interest over potential capital appreciation.

The need for income is rooted in the desire for liquidity and financial flexibility. Regular income from investments can fund daily expenses, support philanthropic endeavors, or be reinvested to compound wealth over time. For many, it provides a sense of security amid market volatility.

At its core, investing involves allocating savings into assets with the expectation of generating a return. This return can come in two primary forms: income and capital appreciation. Income-generating investments, such as bonds and dividend-paying stocks, provide regular cash flow through interest payments or dividends. Non-income-generating assets, like growth stocks or certain commodities, rely on price appreciation, which may require selling the asset to realize gains.

The choice between income and non-income investments often hinges on an investor’s financial goals, risk tolerance, and liquidity needs. Income investments offer the benefit of steady liquidity, making them attractive for those needing regular cash flow. Conversely, non-income investments may offer higher growth potential but require a longer time horizon and comfort with wider market fluctuations.

While the primary objective for most investors is maximizing total return—balancing capital appreciation, dividends, and interest income—there’s significant utility in focusing on income-generating assets. These investments can address specific needs, such as funding retirement expenses or meeting institutional payout requirements, all while managing risk prudently.

Yield: The Heart of Income Investing

Yield represents the income return on an investment, expressed as a percentage of the investment’s cost. It quantifies the cash flow—through interest or dividends—that an investor receives, providing a clear picture of potential income for reinvestment or consumption.

Financial advisors lead clients through detailed discussions regarding assets, liabilities, future goals, legacies, and cash flow needs. Often, the product of this discussion and analysis is the construction of an investment portfolio that aligns risk and return with the investor’s unique circumstances. For the exceptionally risk-averse or extremely well-capitalized, a portfolio of treasury bonds might suffice, offering maximal stability and minimal volatility.

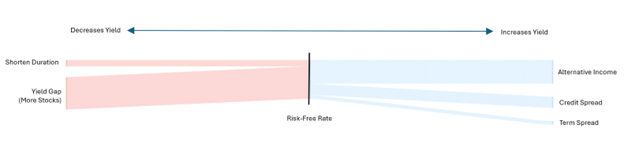

The risk-free rate, often proxied by the 10-year Treasury yield, represents the return on an investment with zero risk of financial loss. Currently, the 10-year Treasury yield is about 4.0%. This may sound decent to some, but typically this yield is not sufficient as a stand-alone investment for long-term investors, particularly when one accounts for inflation.

Investors aiming to increase their portfolio yield beyond the risk-free rate face limited options:

- Increasing Duration (Term Spread): By investing in longer-term bonds, you can earn higher yields, but you’re exposed to greater interest rate risk. If rates rise, the value of these bonds can decrease significantly.

- Decreasing Credit Quality (Credit Spread): Allocating to lower-rated bonds can boost yields but increases credit risk. This strategy requires careful credit analysis to manage the potential for loss.

- Exploring Alternative Income Sources: Assets like Real Estate Investment Trusts (REITs) or employing derivative income strategies (e.g., covered call writing) can offer attractive yields. However, they come with their own set of risks, including market volatility and complexity.

Incorporating equities into a portfolio typically reduces the overall yield due to the “yield gap” between fixed income securities and stocks. Dividend yields on stocks are usually lower than yields on most fixed income investments. While equities offer the potential for capital appreciation, which can enhance total return, they may not contribute significantly to current income.

Due to these dynamics, delivering high-yielding portfolios that also offer the possibility for capital appreciation is inherently challenging. Investors must navigate:

- Risk Management: Balancing the desire for higher yields with acceptable levels of risk, whether from longer durations, lower credit quality, or alternative assets.

- Diversification: Combining various income-generating assets to spread risk while striving for a satisfactory yield.

- Income vs. Growth Trade-Off: Recognizing that higher income today might come at the expense of growth potential, and vice versa.

Our Income Models are designed to address these challenges by offering diversified portfolios that seek to enhance yield while managing risk. By thoughtfully integrating fixed income securities, dividend-focused equities, and alternative income strategies, we aim to provide solutions that navigate the complexities of the current income landscape.

Introducing Our Income Models

To address the nuanced needs of income-focused investors, we are excited to introduce our Income Models: Diversified Income which emphasizes stability, Moderate Income which balances growth and income, and Income & Growth which targets higher growth potential and still delivers significant income generation.

These models are crafted for investors seeking higher expected yields through diversified allocations to bonds, equities, and alternative strategies. Suitable for those with moderate liquidity needs and risk preferences, the models focus on income-generating opportunities and quality over traditional benchmark performance. Below are some key features of the models:

- High-Quality Fixed Income Securities: Providing stable income streams.

- Dividend-Focused Equity Strategies: Targeting companies with consistent dividend payouts.

- Derivative Income Strategies: Such as covered call writing to enhance yield.

- Global Diversification: Including developed and emerging markets to broaden income sources.

- Active Management of Duration and Credit Quality: To optimize income potential while managing risk.

As of August 31, 2024, the estimated total one year return of the Diversified Income, Moderate Income, and Income & Growth portfolios was 6.33%, 7.75%, and 9.62%, respectively.

For the Diversified Income portfolio, the estimated trailing 12-month yield of 5.82% represented 92% of the total return, the Moderate Income portfolio’s trailing 12-month yield of 5.29% represented 68% of the total return, and the Income & Growth portfolio’s trailing 12-month yield of 4.92% represented 51% of the portfolio’s total return.

These income levels showcase the competitive nature of our income-focused solutions, offering meaningful growth opportunities along the efficient frontier.

A Season for Reflection and Action

As you enjoy the rich traditions of fall, consider taking a moment to reflect on your financial goals and the strategies in place to achieve them. Ask yourself:

- Are my investments aligned with my need for regular income and long-term growth?

- Am I effectively balancing risk and return in my portfolio?

- Could a diversified income-focused strategy enhance my financial well-being?

Just as a well-tended orchard can weather storms and continue to produce, a thoughtfully constructed investment portfolio can help you navigate economic uncertainties while pursuing your financial objectives.

We invite you to explore how our Income Models might serve as the foundation for your financial orchard. Together with your Fiduciary Investment Advisor, you can develop a personalized plan that reflects your unique needs and aspirations.