The “golden ratio” is a mathematical concept that has influenced civilizations and cultures for centuries. Its direct influence ranges from the design of the Egyptian pyramids to modern-day database management and encryption.

The first known mention of the golden ratio dates to around 300 BC in Euclid’s Elements and would later become known as the “divine proportion” when Italian mathematician Luca Pacioli’s published his book De divina proportione, in 1509 AD, which included the famed illustrations of Leonardo da Vinci.

So, what is the golden ratio? Interestingly, it has long been considered a symbol of beauty and harmony. It’s favored in art, architecture, and design for its proportions. And its occurrence in nature—evidenced through spiraled galaxies, trees branching, and the human face—produces an effortless familiarity to humans.

In empirical terms, it is a number, a mathematical constant, equal to 1.61803399. The ratio is significant because it is the proportion that divides an object so that the ratio between the whole of the object and its larger portion is equal to the ratio between the larger and smaller portions of the object.

The golden ratio is everywhere. It appears in the design of the Greek Parthenon, arises from Fibonacci sequences in mathematics, and is featured in the modern design layouts of websites and periodicals. It’s virtuosically showcased by Leonardo da Vinci in the Mona Lisa, and even makes an appearance in Gershwin’s arrangement of Rhapsody in Blue. Freddie Mercury’s raucous bridge in the song Under Pressure occurs precisely at its “golden moment.”

The exact reason why the golden ratio is aesthetically pleasing to humans is unclear. Scientists do not agree, however, one explanation mirrors an economic concept called the subjective theory of value, which simply states that value is determined by individual perceptions. In the case of the golden ratio, it may be said that beauty and harmony are shaped by what is prevalent in our experience and natural to us.

It is no surprise that the 60% equity and 40% fixed income (60/40) asset allocation has become a symbol of balance and symmetry in portfolio theory. It is an empirically beautiful and truly harmonious keepsake in the field of portfolio management.

THE HARMONY OF THE 60/40 ALLOCATION

First, let’s focus on the harmony of the 60/40 asset allocation and then we will, in fair warning, take on a very technical approach to discussing the empirical beauty of the 60/40 asset allocation. There are many ways this specific asset allocation elicits harmony.

The 60/40 allocation was developed during the early days of modern portfolio theory as a solution to the challenges faced by institutional investors and large groups of investors, such as endowments or pension funds, whose risk was shared and somewhat difficult to conceptualize. The allocation’s balanced risk profile was viewed as congruent with the average risk profile of the whole and, interestingly, this has proven to be mostly true in today’s age of laser-focused financial and investment planning.

For example, American Trust’s proprietary retirement plan participant managed account solution conducts a quarterly analysis of over 50,000 individual participants and selects an optimal portfolio based on its in-depth review of the participant’s unique funded ratio. On an individual level, the program may select asset allocations ranging from about 30% equities up to about 90% equities, but if you look at the program entirely, the total pool of assets tends to amount to a collective asset allocation of about 60% equities and 40% fixed income. This has been relatively stable for more than a decade.

Another example how the 60/40 allocation elicits harmony in portfolio management is how the allocation can be used by portfolio managers as a benchmark for portfolio optimization across the efficient frontier. Portfolio managers routinely develop an idealized 60/40 asset allocation, often called a “policy portfolio”, representative of their purest risk-balanced ideas and then tweak the allocation across various segments of the efficient frontier to produce allocations optimal to each risk level. While acknowledging there is a place for unique alternative strategies that employ more of a satellite approach, the 60/40 allocation naturally forms a type of gravity that aligns a broad array of cohesive asset allocation strategies from across the risk spectrum.

THE BEAUTY OF THE 60/40 ALLOCATION

It’s difficult to elaborate on the empirical beauty of the 60/40 allocation without getting pretty technical. With that said, investment professionals review vast amounts of investment returns, and the nature of those returns, when constructing investment portfolios. These professionals survey the data, including return distributions for a variety of potential investments, and seek to produce asset allocations that combine those investments in the “best” way. “Best” can mean a variety of things, but most often it means combining investments in a way that maximizes potential return and minimizes potential risk. Risk is commonly expressed as standard deviation, or the variability of returns over time, but there are actually four “moments” in statistics that describe the nature of any investment’s risk and return profile.

- “1st Moment” – The mean is the average return of the investment returns. Higher returns are preferred.

- “2nd Moment” – The variance is a measure of the spread of the investment returns. Lower variance is preferred.

- “3rd Moment” – The skewness is a measure of the asymmetry of the investment returns. Positively skewed returns are preferred.

- “4th Moment” – The kurtosis is a measure of the concentration of returns near the average return. Preferences may vary.

Long-term investors typically utilize equity investments to earn a higher return versus fixed income investments, but this is typically done at the cost of increased risk. If investors can reach their goals without taking additional risk, there would be no incentive do so, but for investors seeking higher returns the goal of a portfolio manager is to deliver those returns with the least incremental risk necessary.

The 60/40 allocation not only feels like a natural and accepted standard for a balanced asset allocation, but the data supports that notion. When looking at long-run return histories, each asset allocation portfolio ranging from 0% equity and 100% (0/100) fixed income all the way to 100% equity and 0% fixed income (100/0) will produce a return distribution with its own unique mean, variance, skewness, and kurtosis.

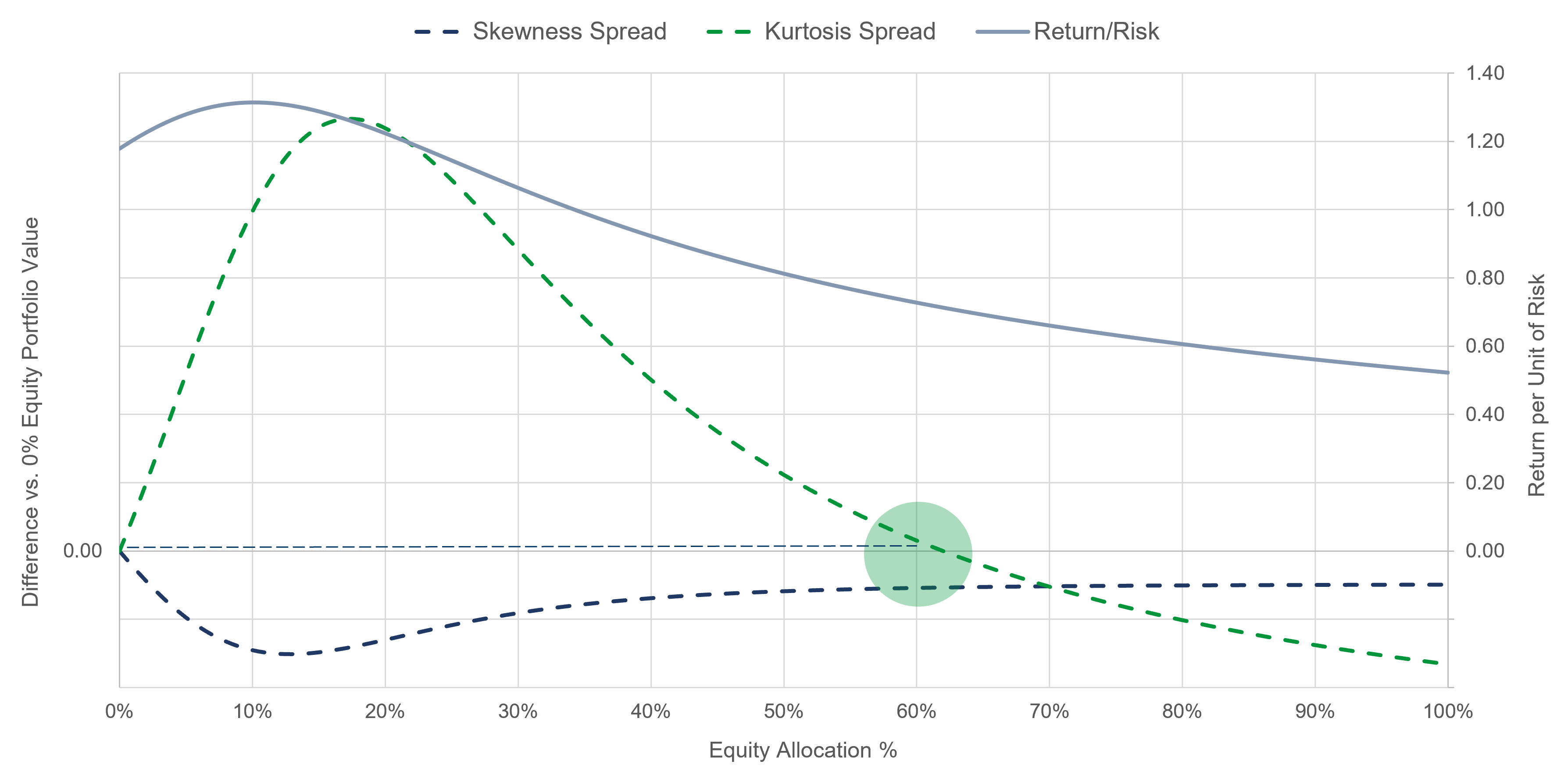

The below chart illustrates the ratio of risk per unit of return for each portfolio along the efficient frontier as well as the spread, or difference, between each portfolio’s measure of skewness and kurtosis and the 0/100 portfolio’s measure of skewness and kurtosis. The red circle captures the point where the ratio of return per unit of risk is highest when the measures of skewness and kurtosis of each incremental portfolio converge closer to those of the 0/100 allocation. As you may notice, this occurs at the 60/40 portfolio.

Simply put, the 60/40 allocation is that portfolio for which the highest level of return is combined with a risk profile commensurate with an inherently less risky 0/100 portfolio across all four “moments” of the return distribution. This is a very technical observation, but sometimes that’s what we do “under the hood.” Regardless, we believe it is sufficient to say that the 60/40 allocation is an empirically beautiful and gilded keepsake in modern portfolio theory as evidenced by the unique balance and harmony of its risk and return profile.

A LESS THAN DIVINE YEAR FOR THE 60/40 ALLOCATION

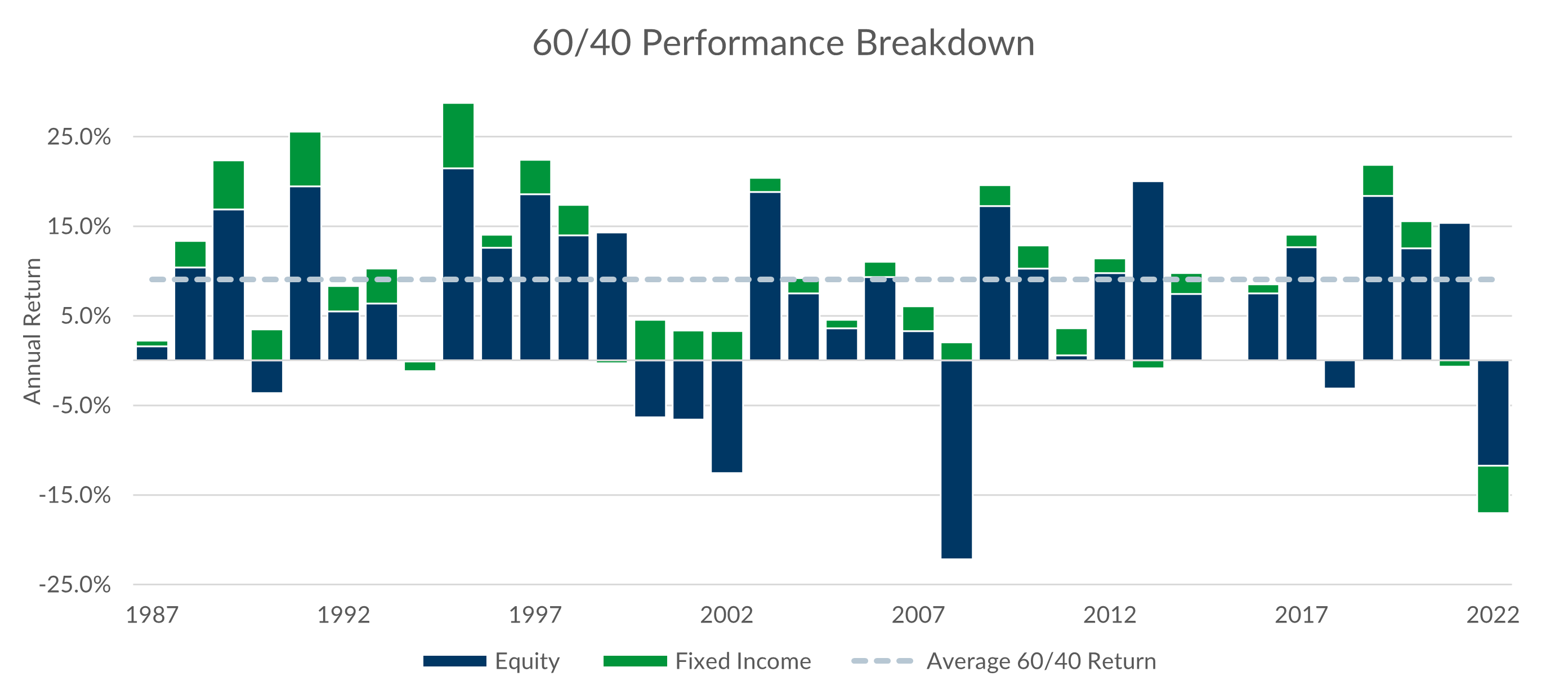

The investment industry loves to illustrate the time-tested performance of the 60/40 asset allocation versus individual, undiversified, asset classes. Typically, the 60/40 allocation will outperform the average asset class in any given year. However, 2022 proved to be one of its most challenging years on record.

It is often said that “the only thing that goes up in a down market are correlations” and this was true last year when both equity and fixed income investments were negative returning -12% and -5%, respectively. This remarkably rare event was a function of complex economic developments such as interest rate hikes fueled by rapid inflation, as well as the powerful effects of duration risk on fixed income investments in a low-rate environment. The below chart illustrates just how much of an outlier 2022 was for the performance of the 60/40 allocation.

Over the past 35 years, the 60/40 allocation has returned an average nominal return of about 9% per year (not adjusting for inflation). The -17% return in 2022 was the worst in over 35 years and one of only two years in which both equity and fixed income asset classes were negative during the same year, the other being in 1994 when the 60/40 returned -1.2%. Granted the market faces imminent and meaningful economic headwinds, but the data is very clear that investors following a methodical, diversified, investment strategy tend to be rewarded when diversifying assets across portfolios with elegant combinations of risk and return.

We certainly hope and believe that in 2023 and beyond the 60/40 asset allocation, along with its many asset allocation cousins spanning the efficient frontier, will snap back to the “golden” returns we have come to expect from meaningfully diversified, sleep-at-night, asset allocation portfolios.

As always, If you have any questions, please don’t hesitate to reach out to your Fiduciary Investment Advisor.